Aluminium consumption saw a modest growth globally (+1% Year- Over-Year) due to stagnant economies curbed by rising interest rates and inflation, ongoing supply chain disruptions and weak consumer confidence. Chinese economy showed signs of stability fueled by resilient manufacturing sector and a rebound in auto sector and consumer goods spending (+ 5% YoY). KSA’s aluminium consumption plunged by 6% YoY, dragging down the demand in Middle East by 7% YoY. US economy is transitioning to a slower pace with labor market easing and consumers facing increased cost pressure due to higher interest rates – this has led to a drop of 6% YoY in aluminium demand. Sluggish EU economy caused by tighter controls on spending, rising prices (high inflation) and weaker consumer interest have led to a contraction in aluminium consumption of 8% YoY.

Global supply rose by a modest 2% YoY. Chinese supply slowed due to winter disruptions in the South (+3% YoY). Production in North America rose by 3% YoY with smelters’ restarts. Supply in the Middle East is almost flat (+1% YoY) with gains in Bahrain & UAE (+1% YoY) offset by a decline in KSA (-6% YoY). Primary production in Europe dropped by 4% YoY due to weak manufacturing activity.

World market without China posts first surplus since 2020 (+51,000 MT) & in deficit with China (-6,000 MT). LME stocks of Russian origin surged to reach 90% of total LME stocks. UK imposed additional sanctions on Russian metal.

LME Cash averaged US$2,252/t in 2023 – down by 17% YoY.

Rolling Ingots

T-Ingots

Mixed Macroeconomic Outlook in 2024: Supply Constraints & Demand Upturn • Global demand is expected to see a gradual rebound in the latter half of 2024 fueled by anticipated Chinese stimulus measures into their economy, prospects of interest rate cuts in the US boosting consumer spending and gradual recovery in Europe as consumption picks up after a sluggish start. • Russian aluminium exports to EU are likely to decline due to expected trade sanctions against Russia diverting exports to Asia particularly China. • US aluminium offtake is projected to grow in 2024 despite anticipated GDP slowdown, mainly driven by investments and expansions in casting, extrusions, and rolling sectors.

• European demand is likely to remain passive in H1 2024 due to stagnant construction activity & high interest rates dampening business and consumer confidence. • Demand in China is expected to expand, despite a weak construction sector, thanks to growth in auto and renewable energy sectors. • Global supply chain challenges have improved, but some risks remain on routes like Panama and Suez Canals. • Bearish market sentiment is likely to persist with LME prices ranging between US$2,000 /t – US$2,200/t.

Properzi Ingots

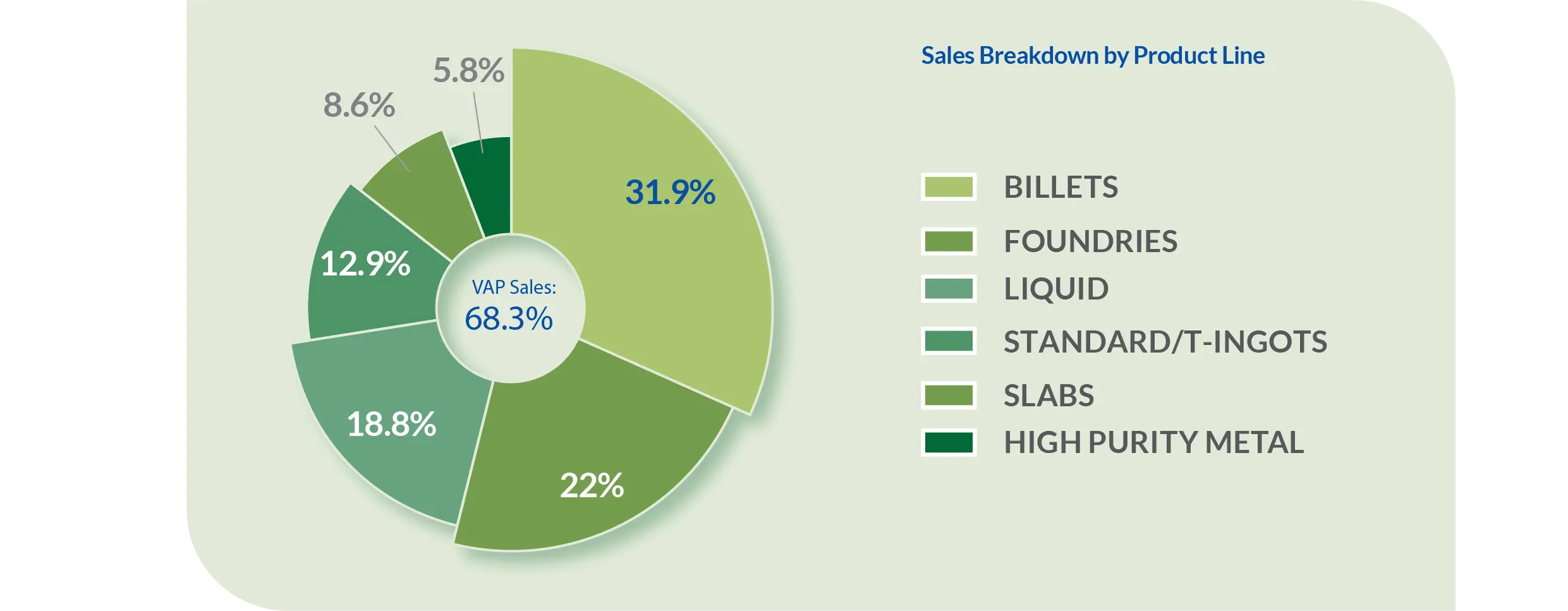

Below are the Sales’ Breakdown by Footprint and Product-Line

Sales by Geographic Footprint

AMERICAS

14.3%

EUROPE

24%

BAHRAIN

26.2%

MENA

20.6%

ASIA

14.9%

73.8%

of Alba products are exported worldwide through its Sales offices in Zurich & Singapore as well as a Subsidiary in Atlanta - US

For more details regarding Alba’s Aluminium Products please scan the QR Code